Differences in Claiming Social Security Retirement Benefits at 62, 67, and 70

By: Lim Chan

June 30, 2025

When it comes to claiming Social Security retirement benefits, age matters. Let’s run some calculations to determine whether someone claiming retirement at age 70 can catch up financially to those who claimed benefits at ages 62 or 67.

For individuals born after January 1, 1960, the earliest age to claim Social Security retirement benefits is 62, the full retirement age is 67, and the age for maximum benefits is 70. At 62, a person receives 70% of their full retirement benefits, as determined by the equation provided by the Social Security Administration (SSA). The benefit is reduced by 5/9 of one percent for each month claimed before reaching full retirement age, up to 36 months. If the reduction exceeds 36 months, the benefit is further reduced by 5/12 of one percent per additional month. At 67, the person qualifies for 100% of their retirement benefits, while at 70, the benefit increases to 124%—reflecting an 8% annual increase.

Let’s assume this person has total indexed earnings of $3.5 million over their 35 highest-earning years (an average indexed salary of $100,000 per year). At full retirement age (67), their monthly Social Security retirement benefit amounts to $3,377.75.

• If they claim benefits at 62, their monthly benefit is: $3,377.75 × 70% = $2,364.43

• If they claim benefits at 70, their monthly benefit is: $3,377.75 × 124% = $4,188.41

Now, let’s convert these figures to annual benefits for easier comparison:

• Claiming at 62: $2,364.43 × 12 = $28,373.16 per year

• Claiming at 67: $3,377.75 × 12 = $40,533 per year

• Claiming at 70: $4,188.41 × 12 = $50,260.92 per year

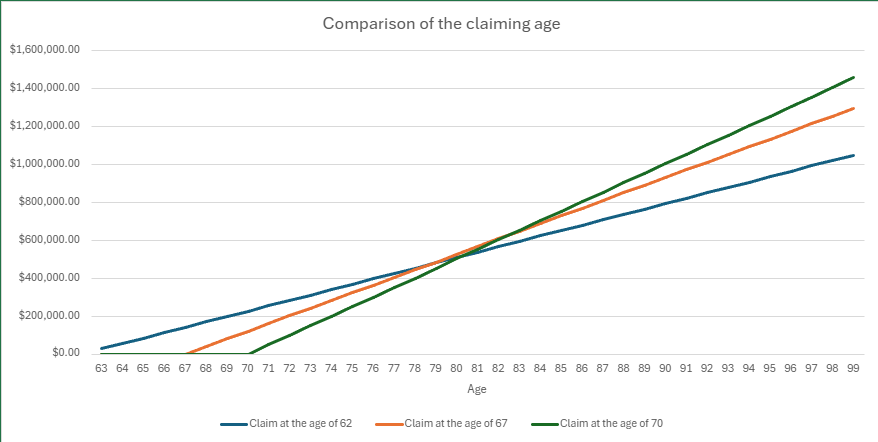

Now, let’s do some calculations. How many years would it take for a person who claimed Social Security at 67 to break even compared to claiming at 62? The calculation is as follows:

5*$28373.16+$28373.16*x=$40533*x. Solve for x (the number of years). x=11.67

This means that by age 67+11.67=78.67, claiming benefits at 67 would surpass the total amount received if benefits had been claimed at 62.

Now, let’s do another calculation. How many years would it take for a person who claimed benefits at 70 to break even compared to claiming at 62 and 67?

For 70 vs. 62:

8*$28373.16+$28373.16*x=$50260.92*x. Solve for x (the number of years). x=10.37

This means that by age 70+10.37=80.37, claiming benefits at 70 would surpass the total amount received if benefits had been claimed at 62.

For 70 vs. 67

3*$40533+$40533*x=$50260.92*x. Solve for x (the number of years). x=12.5

This means that by age 70+12.5=82.5, claiming benefits at 70 would surpass the total amount received if benefits had been claimed at 67.

In conclusion, choosing when to claim Social Security is a crucial decision shaped by factors like financial stability, life expectancy, and employment status. The calculations above serve as a helpful guide, offering insight to support a well-informed choice.